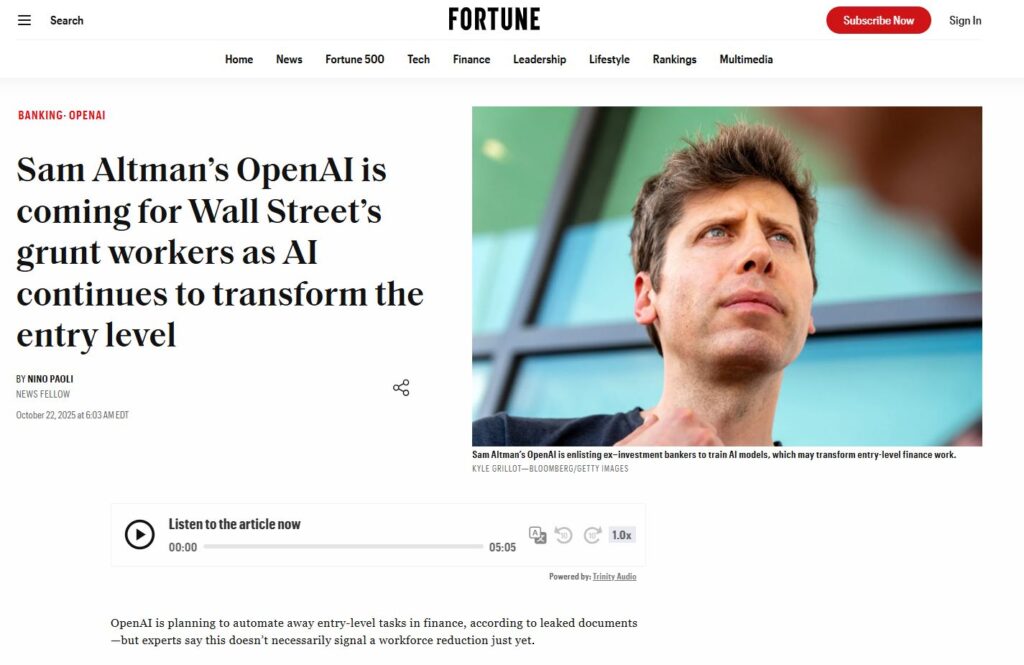

AI in Finance: How Project Mercury Is Redefining Entry-Level Work

A quiet revolution is happening inside the world’s financial institutions. OpenAI’s Project Mercury is bringing together more than 100 former Wall Street bankers to train large language models capable of building financial models on their own. This isn’t about replacing bankers overnight. It’s about redefining what entry-level work means for AI in finance and what […]

Supply Chain Agility: How Mattel’s Q3 Reveals the New Rules of Global Trade

Mattel’s Q3 earnings call this week did more than share financials: it revealed how supply chain agility is becoming one of the most decisive factors in global retail. With tariffs shifting, order windows tightening, and consumer behavior evolving faster than production cycles, agility isn’t just an advantage. It’s the foundation for survival in a volatile […]

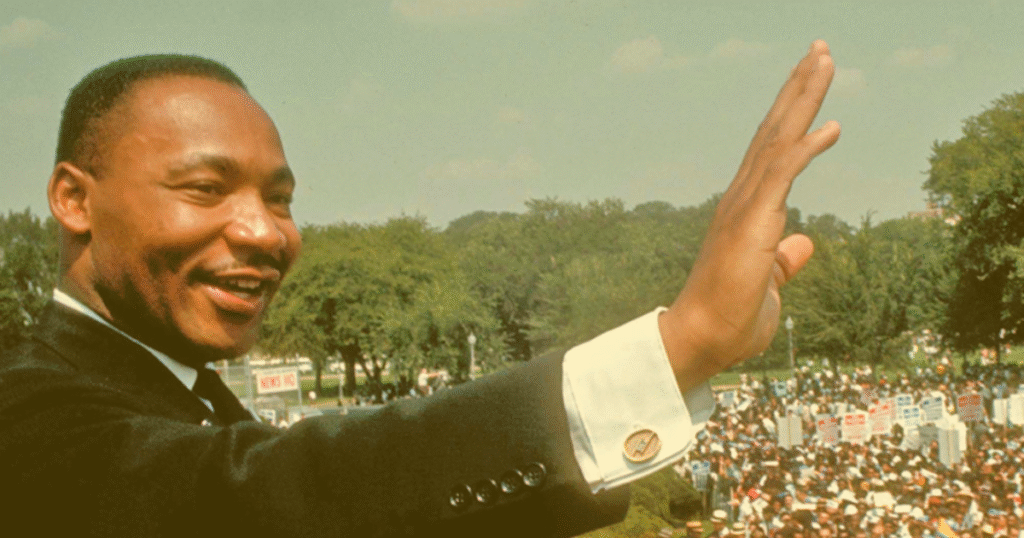

Synthetic Media Regulation: Why Pausing MLK Jr. Depictions Made Sense

Synthetic media regulation is emerging as a key frontier in the age of AI. When Sora 2, the video-generation model from OpenAI, came under fire for unauthorized depictions of celebrities and historical figures, including Martin Luther King Jr., the industry paused and asked how we rebuild rules. Pausing MLK Jr. content was a strong initial signal: […]

Building Your First AI Agent: What Financial Advisors Need to Know

AI agents are entering the mainstream. At their core, these are assistants that can think, act, and execute tasks across multiple apps on your behalf. Their unique advantage is that they combine automation with reasoning, meaning they don’t just follow scripts, they make decisions based on context. That means they can pull data, draft messages, schedule […]

AI in Travel: From Planning to Personalization

AI in travel planning is no longer a fringe experiment. Booking.com’s AI Trip Planner now lets travelers query properties, summarize reviews, and filter intuitively. Expedia is pushing a chat planning app integrating live pricing and inventory directly in ChatGPT. The technology is shortening the path between discovering a trip and actually booking it. In accommodation […]

AI Screen Saver Commerce: The Next Frontier in Smart TV

AI screen saver commerce is becoming real. In a new partnership, Glance and DIRECTV plan to launch AI-generated, shoppable screensavers on TVs in early 2026. Rather than passive wallpaper, your idle screen will turn into a personalized, interactive portal blending content and commerce. This move signals how smart TVs are evolving. Brands need to rethink […]

AI-First Shopping: How Walmart and OpenAI Are Redefining eCommerce

AI-first shopping is no longer a future possibility – Walmart and OpenAI just made it real. With their new collaboration, customers will soon be able to browse, plan, and purchase goods directly inside ChatGPT using Instant Checkout. This move marks a turning point: for two decades, eCommerce was defined by typing into a search bar; […]

DoorDash Delivery Robot: The Future of Autonomous Food Delivery

Robots are no longer a far-off concept, they’re rolling through neighborhood streets. DoorDash Labs has just unveiled an all-electric DoorDash delivery robot designed to bring meals directly from restaurant kitchens to customer doorsteps. The robot stands 4’6”, weighs 350 pounds, and can carry the equivalent of six pizza boxes. It navigates at speeds of up […]

Shein Store Paris: Fast Fashion Meets French Retail

Shein is no stranger to controversy, but its latest move could be its boldest yet. The global fast fashion giant is opening a permanent Shein store in Paris inside BHV Marais, with additional rollouts planned in Galeries Lafayette locations across Dijon, Grenoble, Reims, Limoges, and Angers. For years, Shein thrived as an online-only disruptor, leveraging […]

Agentic AI: Unlocking the Next Chapter of Organizational Transformation

Agentic AI is emerging as one of the most transformative ideas in technology today. Unlike earlier applications of artificial intelligence, which focused on incremental efficiencies, it creates entirely new ways of working. It doesn’t just make processes faster, it rewires organizations and unlocks new economic models. On the other hand, for leaders, this is not […]